In a move that echoes a controversial chapter in India's edtech history, PhysicsWallah (PW) is betting big on student financing.

During the sector's boom years, education loans emerged as a powerful growth lever for startups.

Easy credit helped remove upfront affordability barriers, drive enrolments and support the sale of higher-ticket courses.

The strategy worked, at least for a while. But the model eventually began to unravel. The most prominent casualty was BYJU'S. Its aggressive reliance on third-party lenders to finance expensive courses triggered regulatory scrutiny, customer backlash and allegations of mis-selling. Financing stopped looking like a conversion tool and started looking like a structural risk.

Now, PhysicsWallah is positioning its lending business as a new growth engine. The company believes it can scale education financing while avoiding the pitfalls that ensnared many of its peers.

So, what gives PhysicsWallah this confidence? And can it build a lending business without repeating the mistakes that tarnished edtech's first experiment with credit?

PhysicsWallah's Lending Ambitions

Ahead of reporting its FY26 earnings on Wednesday (May 27), the listed edtech major approved a capital infusion of ₹120 Cr into its wholly owned NBFC arm, FinZ Finance. The company said the move is aimed at expanding access to education loans for students for whom affordability remains a barrier.

In a post-earnings call, PhysicsWallah cofounder Prateek Boob said that FinZ began operation nearly two years ago via external lending partnerships. Over the past two years, PhysicsWallah disbursed education loans of over ₹200 Cr, while keeping NPAs below 1%.

"These are small-duration loans of less than one year," Boob said during the call. Around 70% of these loans were extended to PhysicsWallah students, while the remaining 30% went to external learners.

Encouraged by early traction, PhysicsWallah decided to bring the lending business in-house through FinZ Finance, which received an NBFC licence in September 2025 and commenced operations in March earlier this year.

The company said that the NBFC licence will improve affordability and access for students from lower-income households. Its management also stressed that PhysicsWallah does not intend to deploy significant capital into the business despite the loans sitting on its own balance sheet.

The business rationale is straightforward. However, the sector's history with education financing raises legitimate questions about whether the model can scale sustainably.

Before examining those concerns, it is worth noting that PhysicsWallah is entering the lending business from a position of strength. With a healthier balance sheet and improving profitability, the company appears to view financing as a calculated risk aimed at unlocking its next phase of growth.

A Strong FY26 Gives PhysicsWallahRoom To Experiment

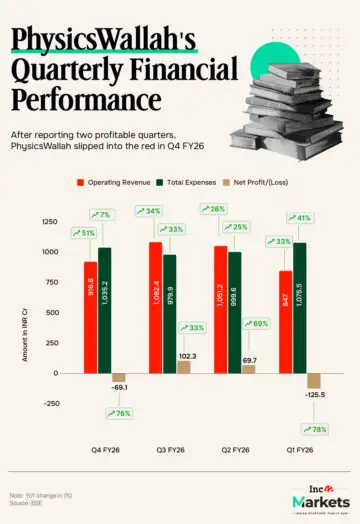

In FY26, PhysicsWallah managed to slash its net loss by 90% to ₹24.2 Cr from ₹243.3 Cr in FY25. Operating revenue surged 35% YoY to ₹3,899.5 Cr.

Consolidated EBITDA more than doubled to ₹549 Cr, while profit before tax stood at ₹10 Cr against a loss of ₹259 Cr in FY25.

The company's online business remained the primary growth engine, with its revenue growing 39% YoY to ₹1,954 Cr in FY26. More importantly, growth is increasingly coming from outside the company's traditional JEE-NEET franchise.

As per Boob, the revenue from state board programmes surged 9X YoY during the year, while Curious Junior - PhysicsWallah's K-8 platform - grew 4X. Foundation, CUET and UPSC categories also gained traction as the company continued diversifying away from its dependence on engineering and medical entrance preparation.

Following a strong FY26, the management now expects overall revenue to grow 30% in FY27, alongside a 2X increase in pre-Ind AS EBITDA.

The company has also recalibrated its capital allocation priorities. During the call, Boob said PhysicsWallah has pivoted its K-12 expansion strategy away from a capex-heavy model of setting up schools toward an asset-light approach centred around state boards, school integration partnerships (SIPs), and online-first categories.

Under the SIP model, the company partners with schools and deploys faculty and curriculum infrastructure inside existing campuses instead of building schools outright. According to the management, revenue from SIPs tripled during FY26.

Simultaneously, the Alakh Pandey-led company seems to have sharply moderated its earlier appetite for acquiring and operating schools directly. Instead, the management now appears focused on improving returns from the company's existing offline network.

Offline Business Gains Momentum

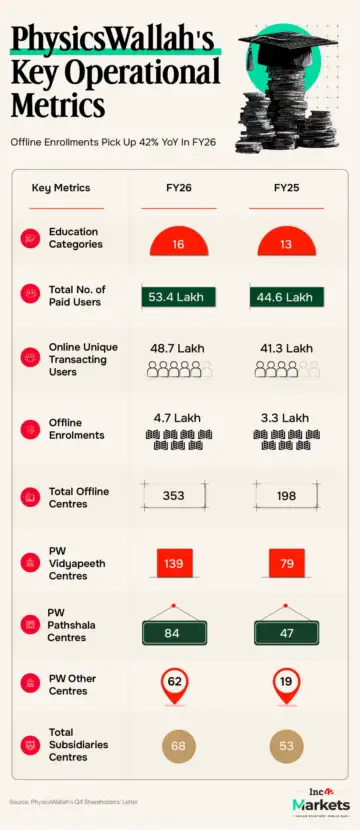

The company's offline vertical also saw strong growth in the last fiscal year. Its offline centre count increased to 353 from 198 at the end of FY25, while offline revenue grew 31% YoY to ₹1,774 Cr. The revenue from the offline segment accounted for 45% of the total operating revenue during the year.

According to the management, nearly 60% of its Vidyapeeth centres are now profitable, while centres opened in 2023 and 2024 have already turned EBITDA positive. Offline EBITDA margins improved to -10% in FY26 from -19% in FY25.

The company now expects its offline business to turn profitable at a group level in FY27. "We are very confident of achieving PAT-level profitability in FY27," Boob said.

While increasing offline centres can be a concern in terms of losses, Anand Rathi Investment Banking's executive director Atul Thakkar believes PhysicsWallah's course diversification push is aimed at reducing the risks associated with running a large offline coaching network dependent on a handful of exam categories.

"An offline centre built purely around JEE or NEET coaching is a high fixed-cost asset tied to one exam cycle. What makes PhysicsWallah's strategy more defensible is that management appears conscious of this risk and is diversifying accordingly across state boards, commerce, vernacular content and K-12," he said, adding that investors should view it "less as an edtech company with centres and more as an education institution with strong digital delivery capabilities".

But as PhysicsWallah expands into higher-ticket offline offerings through its Vidyapeeth centres, state board programmes and premium online courses, affordability will increasingly emerge as a key challenge, particularly in Tier II & III markets.

This is where FinZ Finance enters the picture.

Can FinZ Unlock The Next Leg Of Growth?

Financing helps smoothen conversion friction without forcing the company to discount products. Thakkar believes FinZ has the potential to become a meaningful monetisation lever over the next few years.

"At 10-12% loan penetration over the next two to three years, FinZ becomes a material contributor to revenue per student and to conversion on premium products," he said.

He also argued that PhysicsWallah possesses a structural underwriting advantage unavailable to traditional lenders. "Credit risk is better understood here than in conventional consumer lending. Borrowers are already enrolled students. Repayment behaviour can be correlated with course completion and outcomes."

This advantage becomes particularly relevant because many PhysicsWallah users come from first-time borrower households with limited formal credit histories. Traditional lenders typically either reject such customers or price loans aggressively. PhysicsWallah, meanwhile, believes its student engagement and academic performance data can help underwrite these borrowers more effectively.

The model makes strategic sense on paper. But India's edtech sector has already demonstrated how quickly education financing can become a liability.

No matter how PhysicsWallah frames its NBFC ambitions, comparisons with BYJU'S are inevitable. The poster child of India's edtech boom relied heavily on partnerships with fintech lenders during its years of aggressive expansion to finance high-cost tablet-based learning programmes. While the model helped drive enrolments, it later drew widespread criticism over alleged mis-selling, coercive recovery practices and mounting debt burdens on families.

The fallout significantly eroded trust in edtech financing models.

PhysicsWallah's structure is clearly different. Unlike BYJU'S, the company owns the NBFC directly instead of relying on external fintech partnerships. But the deeper concern is not regulatory architecture, it is incentive alignment.

According to Thakkar, the key risk is what happens when the same institution controls both admissions and financing.

"Running an NBFC alongside edtech creates an inherent conflict between the interest of the lender and the interest of the educator. When the same entity that profits from enrollment also controls the financing that enables enrollment, the incentive structure can get distorted," he said.

"This is not a hypothetical, it is exactly what went wrong for some of PhysicsWallah's peers. Regulatory scrutiny on this specific dynamic is only going to intensify, and management will need to demonstrate a clean operational firewall between FinZ and the core business consistently," Thakkar added.

Why Investors Are Nervous

History suggests financing can gradually reshape how education businesses operate. Admissions teams begin prioritising financing-eligible courses. Loan approvals become embedded inside counselling conversations. Growth targets start influencing underwriting quality. And, eventually, financing shifts from being an affordability tool to becoming a demand-generation mechanism.

This has triggered some caution from brokerages as well. Earlier this week, JM Financial downgraded PhysicsWallah from 'Buy' to 'Add', partly citing concerns around the NBFC investment creating an "overhang" on the stock.

The brokerage raised questions around capital allocation discipline and the long-term implications of PhysicsWallah deploying shareholder capital into student lending.

To be fair, the company's current exposure remains relatively modest. The initial ₹120 Cr capitalisation is minuscule compared to its treasury of ₹5,027 Cr at the end of FY26. The management repeatedly stated that the company does not intend to deploy "significant capital" into lending.

But lending businesses rarely stay small if they work. If FinZ materially improves offline conversion and drives uptake of premium offerings, the incentive to scale its loan book aggressively could increase significantly.

This is where discipline will be critical. Whether FinZ becomes a competitive advantage or a future headache will depend on execution. PhysicsWallah's challenge will be to continue behaving like an education company while simultaneously operating like a lender.

MARKETS WATCH: NEW ISSUES, POST-IPO JOURNEY & MORE

- Pine Labs' First Profitable Fiscal: The fintech major remained profitable throughout FY26, recording an uptick in its profit throughout the fiscal. In Q4 FY26, Pine Labs reported a net profit of ₹59.4 Cr as against a loss of ₹28.9 Cr in the year-ago quarter, while its operating revenue rose 15% YoY to ₹700.5 Cr.

- Swiggy To Reattempt IOCC Bid: The foodtech major has disclosed that it is actively engaging with shareholders after failing to secure enough votes to amend its AoA and become an Indian-Owned and Controlled Company, a status crucial for shifting Instamart to an inventory-led model.

- Another Regulatory Win For MobiKwik: Marking a second key approval within a week, MobiKwik has received the RBI's in-principle nod to operate as a physical payment aggregator-physical (PA-P). The clearance allows the company to pursue business expansion in offline merchant business.

- PB Fintech Cofounders Dump Shares: Cofounders Yashish Dahiya and Alok Bansal sold 38 Lakh shares of the company via multiple block deals for a cumulative sum of ₹665.4 Cr. The shares were picked up by Goldman Sachs, Morgan Stanley, Societe General, Kotak Securities, Tata Mutual Fund, BNP Paribas, among others.

- FirstCry Trims Q4 Loss: The omnichannel kidswear brand managed to trim its quarterly net loss by 57% YoY to ₹48.2 Cr. However, operating revenue grew 12% YoY to ₹2,162.7 Cr in Q4. For the full FY26, the company's net loss reduced 23% YoY to ₹203.7 Cr while its top line increased 12% YoY to ₹8,547.9 Cr.

Edited by Vinaykumar Rai

Creatives by Varshita Srivastava