Neobank Fi Money is restructuring its business and moving away from some of its consumer-facing products to focus on AI and enterprise technology, cofounder Sujith Narayanan said.

The move comes at a time when Fi is short on cash and rethinks where it can build a sustainable business. As part of the reset, the Bengaluru-based startup will sunset some products and cut roles across teams.

Fi started as a digital-first consumer banking platform and gained early attention for its design-led app, savings tools and fraud protection features. However, not all of its bets worked out as planned, Narayanan said in a LinkedIn post.

Following a review, Fi has now decided to focus on building AI-driven systems for startups and large enterprises, marking a clear shift towards a B2B model.

"This is not about effort or talent. It's about how the company needs to be structured going forward," Narayanan wrote, while saying the transition will be handled with support for impacted employees. However, he didn't disclose the number of employees that would be impacted.

Fi's reset comes after years of weak monetisation and stalled growth in its core lending business. Once positioned as a digital-first banking app for young Indians, Fi has been grappling with slow revenue growth, high burn and repeated product cutbacks.

Last year, Inc42 reported that Fi's lending segment, which was its main revenue driver, was scaled back sharply.

While the startup earlier claimed to be building its own NBFC infrastructure, Inc42 found no evidence of it holding an NBFC licence. At the time, the startup continued to operate as a loan distributor for RBI-registered lenders, a model that has proven hard to scale.

Fi's Struggles & Shrinking Runway

Founded in 2019 by Narayanan and Sumit Gwalani, Fi has raised around $137 Mn to date from investors including Peak XV Partners, Ribbit Capital, Alpha Wave and Temasek. In its early years, the startup spent heavily to acquire users, particularly during the Covid-led surge in digital lending. In FY23 alone, Fi spent ₹132 Cr on marketing.

By 2023, Fi had over 3 Mn users, largely driven by instant personal loans. However, most non-lending products like mutual funds, US stock investments and rewards programmes failed to generate meaningful revenue. This pushed the startup into a cycle of high burn and constant user acquisition.

This resulted in downsizing. Last year, Inc42 reported that Fi laid off over 50 employees, bringing its total workforce to under 100 as of July 2025. Fi's runway fell from around 18 months in December 2024 to about 10 months by March 2025. The startup has not raised fresh capital since.

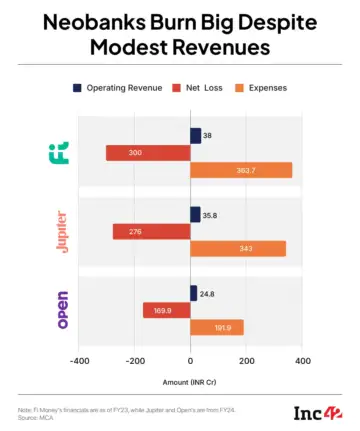

Fi is also yet to file its FY24 and FY25 financials, after reporting a net loss of ₹300 Cr on an operating revenue of ₹38 Cr in FY23.

The troubles spilled over to customer experience. Users complained about delayed refunds and slow support - issues worsened by Fi's dependence on Federal Bank and multiple third-party service providers. Tighter RBI rules on digital lending and rising competition from banks' apps like SBI YONO and Kotak 811 added further pressure.

Fi's struggles underline the broader challenge facing India's neobanks - none of which are profitable. For Fi, the pivot marks a bid to survive in a market where the original promise of neobanking is increasingly wearing thin.