Foodtech major Swiggy saw its loss rise for yet another quarter in Q1 FY26 as it continued to invest to expand its quick commerce operations.

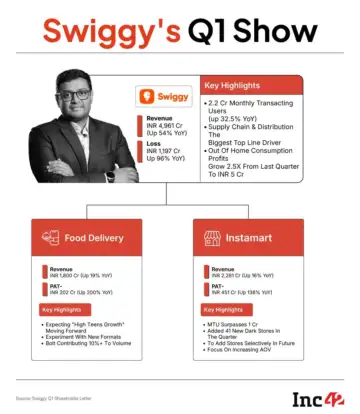

The company's net loss zoomed 96% to INR 1,197 Cr in the June quarter from INR 611 Cr in the year-ago quarter. On a sequential basis, the company's loss grew 11% from INR 1,081 Cr.

However, Swiggy's top line saw strong growth. Operating revenue surged 54% to INR 4,961 Cr in Q1 FY26 from INR 3,222 Cr in the year-ago period. On a QoQ basis, this marked a 12% increase from INR 4,410 Cr.

The company's adjusted EBITDA loss increased 75% YoY to INR 813 Cr from INR 465 Cr in Q1 FY25. On a QoQ basis, this figure increased by INR 81 Cr.

Including other income of INR 87 Cr, total income for the quarter zoomed 53% YoY to INR 5,048 Cr.

Meanwhile, expenses rose 60% on a YoY basis. Total expenditure stood at INR 6,244 Cr during the quarter under review from INR 3,908 Cr a year ago. Sequentially, this was a rise of 11% from INR 5,610 Cr.

Swiggy divides its business into four segments - food delivery, quick commerce, supply chain and distribution, and platform innovations. Here's how the segments performed during the quarter.

Supply Chain & Distribution: Under this segment, Swiggy leverages its warehousing capabilities to offer supply chain services to FMCG brands. It is the main driver of Swiggy's top line, bringing in a revenue of INR 2,259 Cr during the quarter. This was an increase of 78% YoY. The segment's loss also increased slightly to INR 47 Cr from INR 43 Cr in the year-ago quarter.

Food Delivery: The segment reported a relatively muted growth. Its operating revenue zoomed 19% YoY to INR 1,800 Cr, while profit rose 200% YoY to INR 202 Cr.

Quick Commerce: Instamart continued to weigh on the company's bottom line for yet another quarter. The segment's loss stood at a staggering INR 797 Cr in Q1 FY26, almost 3X of INR 280 Cr loss in the year-ago quarter. Its revenue grew over 2X to INR 806 Cr from INR 374 Cr in Q1 FY25.

Platform Innovations: This segment, which houses Swiggy's supplementary businesses like Swiggy Sports, SNACC, among others, raked in a revenue of INR 20 Cr and posted a loss of INR 52 Cr during the quarter.

Out of Home Consumption: The company continued to mint profits from its DineOut and SteppinOut offerings in Q1 FY26. After turning profitable in the previous quarter, the vertical's profits rose to INR 5 Cr this quarter as against a loss of INR 13 Cr in the previous year quarter. Operating revenue grew 67% YoY to INR 77 Cr.

"Swiggy's food delivery business continues to deliver robust growth, while innovating to create new customer propositions which can open up the market further… We have moved past the March 2025 peak of losses in quick commerce, but amidst significant competition we will modulate investments to ensure that we drive the business towards scale-led profitability," Swiggy cofounder and group CEO Sriharsha Majety said.

Overall, Swiggy's monthly transacting users grew 32.5% YoY to 2.2 Cr during the quarter. The company served 2.6 Cr B2C orders in the quarter, a 24% YoY spike from 2.1 Cr orders served in the previous year's quarter. However, platform frequency, which is defined as completed orders per user in a month, slipped to 4.2 in Q1 FY26 from 4.5 orders per month per user in Q1 FY25.

Now, let's take a detailed look at the Q1 performance of Swiggy's flagship consumer facing verticals.

Food Delivery

Swiggy's food delivery gross order value (GOV) rose 18% YoY and 10% QoQ to INR 8,086 Cr during the quarter. While the segment's adjusted EBITDA zoomed over 2X YoY to INR 192 Cr, the number fell by INR 20 Cr from the previous quarter. Contribution margin also dipped from 7.8% in the last quarter to 7.3%.

The company said that the QoQ dip came due to higher delivery costs as there is a dearth in availability of delivery partners during the June quarter. Important to note that Swiggy's competitor Eternal also said that there was lower availability of delivery partners in Q1.

Also similar to Eternal, Swiggy expects a "high-teens growth" in its food business in the near-term as "newer use-cases gain consumer traction".

To sustain growth in the segment, the company is working with its partners to figure out models that allow it to deliver more functional meals to its customers. Notably, Swiggy has been experimenting with new segments like a high-protein food category, meals under INR 99, among others.

A key highlight in Swiggy's food delivery experiments has been its 10-minute delivery service, Bolt. Swiggy said that the offering contributes over 10% to its overall food delivery volumes. At the end of the June quarter, Bolt had "fully-scaled" to across 500+ cities.

"However, the lower last-mile reduces delivery costs, making Bolt economics similar to the overall platform. As the only such service in the market, it also creates differential salience for our platform across both consumers and restaurant partners," the company said.

Quick Commerce

Continuing the expansion spree, Swiggy added 41 new darkstores during the quarter to take its total store count to 1,062. With higher penetration, Instamart's total orders stood at their highest at 9.2 Cr in the three months, while average order value grew 26% YoY to INR 612. However, the orders served by darkstore per day shrunk 17% QoQ and 14% YoY to 985.

Despite Majety claiming that Instamart has moved past its March 2025 peak of loss, its loss increased by INR 26 Cr from last quarter. The adjusted EBITDA loss of the vertical also rose 7% QoQ to INR 896 Cr.

The company said that the rise in loss was because of it ramping up its Maxxsaver feature, which guarantees users additional savings for large orders. Besides, seasonal investments into delivery partners was also a factor for the increase in loss.

Maxxsaver was launched at the start of Q1 and Swiggy claims that it has been a success, helping it increase wallet-share per user. However, it also led to "cart consolidation", resulting in a slightly lower number of orders by the same user.

Shares of Swiggy ended today's trading session 0.62% higher at INR 403.80 on the BSE.