While the overall investment sentiment remained largely stable in the first half of 2026 (H1 2026), investor appetite for late stage startups remained subdued.

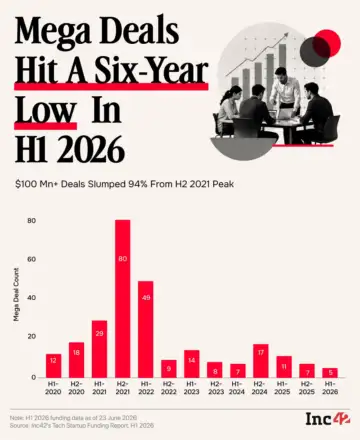

This was particularly evident in the number of mega funding rounds during the period. Only five startups - CRED, Rapido, Spinny, Sarvam and KreditBee - secured funding rounds exceeding $100 Mn.

As per Inc42's 'Indian Tech Startup Funding Report H1 2026', the number of mega deals declined 55% from 11 recorded in H1 2025. The mega deal count decreased 29% from 7 such deals in the second half of 2025.

Overall, late stage funding declined 29% to $2.2 Bn during the period under review from $3.1 Bn in the same period last year. Median ticket size also plunged 68% YoY to $10 Mn.

On the contrary, early and growth stage funding in H1 2026 saw an uptick with 18% and 15% YoY jump, respectively.

Geopolitical instability and overall macroeconomics pressure was one of the major reasons for the mega deal drought in the first quarter of 2026. The same instability persisted in the following three months ended June.

Besides, greater investor discipline and evolving investor expectations were among the key factors weighing on India's mega funding landscape.

Let's take a detailed look at the exact reasons behind this decline.

The Profitability Push And Liquidity Reset

Against the backdrop of shifting geopolitical dynamics and a maturing Indian startup ecosystem, one thing is clear - investors are no longer willing to fund growth at any cost.

Alkemi Growth Capital's partner Mansi Aggarwal outlined how investor sentiment has shifted from a growth-first mindset to a more disciplined approach, with revenue quality, visibility into profitability, and governance now sitting at the intersection of late stage investment decisions.

The shift has been driven in part by a series of governance lapses over the past few years. Widely reported instances of founders misrepresenting financials and startups repeatedly raising capital without demonstrating sustainable fundamentals have made late stage investors far more discerning.

Meanwhile, Celesta Capital managing partner Sudhir Rao attributed the mega deal slowdown to the natural evolution of the funding cycle. Late stage investors typically operate within defined holding periods, and as their portfolios mature, the focus shifts from deploying fresh capital to generating exits.

The timing supports this view. H2 2021 marked the peak of the Indian startup funding boom, with 80 mega deals. As late stage funds generally have investment horizons of five to eight years, many investors who deployed capital during that period are now likely prioritising liquidity events over writing new mega cheques.

"We have to look at what the typical holding period of late stage ownership has been. If that period is being crossed, investors are now looking for either an M&A event or an IPO. And if a large number of IPOs are taking place, that activity is naturally absorbing the late stage entities. So one reason could simply be that we're in a stall phase of the cycle," Rao added.

The Red And Green Flags Behind Mega Deal Slowdown

Mega deals don't happen in isolation. They rely on a steady supply of companies graduating from the growth stage. If startups that have already raised Series B or C funding rounds fail to scale as expected, the pipeline feeding late stage funding inevitably weakens.

"If growth stage companies get stalled, the pipeline feeding into mega rounds thins out," Rao added.

Adding to the slowdown, many late stage startups are increasingly turning to the public markets instead of private capital to fund their next phase of growth. However, the first six months of 2026 proved far from ideal for IPO-bound companies.

Several startups, including Flipkart, PhonePe, Curefoods and Captain Fresh, deferred their listing plans amid volatility in the Indian equity markets and concerns over potential valuations.

While the move to delay the IPO was prudent in an uncertain market, it also disrupted the venture capital cycle. IPOs have traditionally been the preferred exit route for late stage investors. When listings are delayed, liquidity events are pushed back, leaving investors with less capital to redeploy in new mega funding rounds.

"Since M&A activity has declined and the IPO market has tempered, it has a trickle-down effect on new investments. When public market exits get harder for the larger players, late stage rounds automatically decline," Alkemi's Aggarwal added.

Another factor could be that many growth stage startups have significantly improved their unit economics over the past 12-18 months. As operating leverage kicks in and businesses become more self-sustaining, the urgency to raise large external rounds naturally declines.

Going ahead, Aggarwal believes deeptech and manufacturing sectors, which historically attracted limited venture capital, to account for a larger share of mega funding rounds.

"India is seeing good-quality assets emerge, and manufacturing requires significant capital - setting up large plants, building export capacity. Founder ambition is also shifting. The idea that India can become a world-class manufacturing and export hub is becoming more serious, and investor interest is following," she added.

Rao, meanwhile, believes sectors that align with India's strategic priorities, including infrastructure, defence tech, aerospace, space tech, AI infrastructure, among others, will attract investor interest.

The shift is already underway. Two of the five startups that entered the unicorn club this year - Sarvam and Skyroot - operate in frontier technology segments. Moving forward, startups like Emergent and Pixxel are also in talks to raise major rounds at significant valuations.

Edited by Akshit Pushkarna