In the world of Indian business mythology, few stories shone as brightly as that of Rajesh and Prashanth Mehta - two brothers from Gujarat who turned a modest family jewellery business into what they claimed was the world's largest gold processing empire.

Their 2015 acquisition of Swiss refinery Valcambi SA for $400 million was the crowning moment. India, it seemed, had a gold king. Today, that crown lies in the dust.

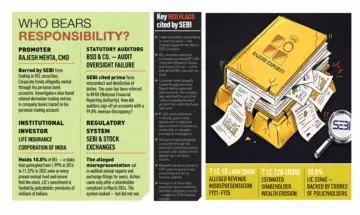

On June 2, 2026, the Securities and Exchange Board of India issued an interim order that has stunned India's financial establishment. SEBI alleged that Rajesh Exports Limited (REL) misrepresented revenues to the tune of ₹15.15 lakh crore - roughly $159 billion - over just five financial years, accounting for 99.8% of the company's consolidated subsidiary revenues. This is one of the most extraordinary figures ever cited in Indian securities regulation. The company's shares fell 5% in a single morning and have lost more than 40% in value this year.

REL has denied wrongdoing. Chairman Rajesh Mehta called the allegations untrue. The company attributed the discrepancy to SEBI allegedly considering Valcambi's EBITDA instead of revenue. But SEBI has held firm, barring Mehta from trading in REL securities and ordering a fresh forensic audit. The damage to investor confidence, shareholder wealth, and India's corporate governance reputation has already begun.

How the Alleged Misrepresentation Occurred

At the heart of SEBI's case is a single, devastating number mismatch. Between FY2020 and FY2024, REL and its Swiss holding company Global Gold Refineries AG (GGR) reported consolidated revenues exceeding ₹15 lakh crore. Valcambi SA - the flagship Swiss gold refinery that was, according to REL, the primary revenue engine of the entire group - independently reported total revenue of just ₹3,027 crore over the same period. That is less than 0.5% of the figure reported above it in the corporate chain.

SEBI described this discrepancy as 'egregious and unheard of' - an unusually blunt choice of words for a securities regulator known for careful, measured language. The regulator further found that between 97-99% of REL's consolidated revenues flowed through overseas subsidiaries, with the Swiss chain at the centre.

The corporate structure itself created an environment where verification was maximally difficult. Valcambi SA is owned by European Gold Refineries, which is owned by Global Gold Refineries AG, which is 95% owned by REL Singapore PTE Ltd. and 5% by REL India. This layered cross-border web meant that any discrepancy between what Valcambi actually earned and what was reported up the chain was extremely hard for external parties - auditors, analysts, regulators - to independently trace.

The probe was formally triggered in March 2024 when a shareholder complaint alleged potential misrepresentation of financial information, specifically pointing to trade receivables that had remained outstanding for more than two years - a significant red flag. SEBI appointed an investigating authority later that year and commissioned BDO India Services Pvt. Ltd. as the forensic auditor.

Why It Went Undetected - A Systemic Governance Failure

The more unsettling question is not merely what allegedly happened, but how it could have persisted - through annual audits, stock exchange filings, analyst research coverage, and institutional due diligence - for nearly five financial years, if not longer.

SEBI's order paints a picture of systemic obstruction. When investigators sought basic records - customer details, supplier ledgers, inventory data, party-wise debtor and creditor lists - they were repeatedly turned away. The company cited Swiss data protection laws and confidentiality arrangements. SEBI flatly rejected those arguments, holding that foreign privacy provisions are designed to protect individuals, not corporations, and that they cannot override disclosure obligations under Indian securities law.

Even where records were eventually produced, forensic auditors found them incomplete and insufficient for transaction-level verification. Access to ERP systems - which would have enabled independent validation of individual transactions - was allegedly denied entirely. The result was what analysts now describe as an 'information black box': aggregate revenues were reported to investors while underlying transactions remained beyond independent reach.

Perhaps the most candid indictment came not from regulators but from the market itself. Domestic mutual funds - institutions that employ entire teams of analysts to scrutinise corporate numbers - had reduced their exposure in REL to precisely zero over the past decade. 'We were never confident of their numbers,' said the CEO of one leading mutual fund. The CEO of a major broking firm was even blunter: 'Huge turnover and thin margins never made sense. Few domestic institutional investors trusted the numbers.' The SEBI order, he added, 'did not come as a shocker.'

The question this raises is pointed: if professional fund managers saw reason for scepticism, why did SEBI, stock exchange surveillance systems, and statutory auditors not trigger an investigation years earlier?

The possible impact

For ordinary investors, the consequences are already visible. SEBI estimates shareholder wealth erosion at ₹12,726 crore. LIC, the single largest domestic institutional holder at 10.8%, faces the most significant domestic institutional exposure - and since LIC's investments are funded by policyholder premiums collected from millions of Indians, the fallout extends well beyond trading floors and stock portfolios.

Canara Bank has reportedly classified its exposure to REL as a stressed asset following repayment defaults and has initiated auction proceedings for outstanding dues of approximately ₹509 crore. Other lenders with REL exposure are watching the proceedings with understandable anxiety.

The reputational damage to Indian capital markets may extend further. Foreign portfolio investors held 17.7% of REL as recently as March 2023; that has dropped to 14.2% in March 2026. The message this episode sends to global investors - that a company listed on India's premier exchanges, audited by professional firms, and covered by analysts could allegedly operate an information black box at this scale - is one India's regulators will need to work hard to counter.

There are also international dimensions. Valcambi is a globally respected Swiss refinery. If the allegations are ultimately proven, the governance questions that arise at one of the world's largest gold refining operations will reverberate across global commodity markets.

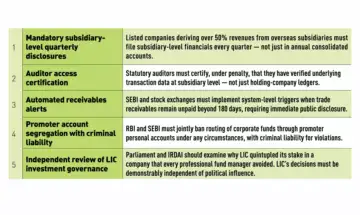

What must be done now - five governance reforms

The fresh forensic audit ordered by SEBI must proceed without obstruction, with investigators granted unrestricted access to ERP systems, primary accounting records, and party-level transaction data across all subsidiaries. REL's invocation of Swiss data protection laws must not be permitted to delay proceedings further. SEBI has already established the legal principle: foreign confidentiality provisions cannot override Indian statutory disclosure obligations.

A question of systemic trust

The Rajesh Exports case is not, ultimately, just the story of one company or one promoter. It is the story of a system that looked but did not see - or perhaps, in some quarters, chose not to look closely enough. Annual reports were filed. Accounts were audited by BSD & Co. and signed off. Disclosures were regularly made to stock exchanges. Analysts published research. And yet, if SEBI's preliminary findings hold, a misrepresentation of truly extraordinary scale allegedly persisted for years.

The parallels to the Satyam scandal of 2009 are uncomfortable and unavoidable. In that case too, the fraud sat in plain sight in audited accounts - until it didn't. What Satyam did for IT sector governance scrutiny, the Rajesh Exports case may do for listed companies with complex cross-border commodity trading structures.

SEBI's findings remain preliminary and interim. Rajesh Mehta and REL will have the full opportunity to present their defence - and the company has maintained that the discrepancy cited by SEBI reflects a misreading of Valcambi's EBITDA rather than its revenue. That defence will be tested rigorously in the proceedings ahead.

But regardless of how the legal case concludes, this episode has already raised a question that India's regulators, auditors, institutional investors, and policymakers must answer honestly and urgently: How robust is the system that is supposed to guarantee the integrity of what Indian investors are told? The answer, this case powerfully suggests, demands immediate and serious reform.