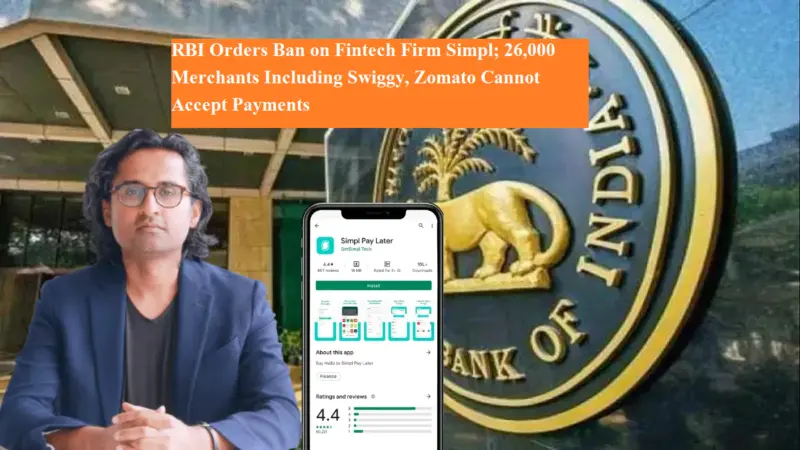

The Reserve Bank of India (RBI) has ordered Bengaluru-based BNPL (Buy Now, Pay Later) company Simpl to immediately halt its payment operations.

The company, which works with over 26,000 merchants, including major platforms like Swiggy and Zomato, was operating a payment system without RBI approval, violating the Payment and Settlement Systems Act, 2007.

RBI Tightens Grip on Digital Credit

This move is part of RBI's broader push to regulate digital credit. BNPL schemes have grown rapidly in recent years, offering instant credit to consumers and easy sales for merchants. However, RBI has expressed concerns over unsecured lending, lax monitoring, and consumer protection. In 2022, the central bank had already barred BNPL companies from topping up prepaid payment instruments with borrowed funds.

Allegations Against Simpl

Simpl is operated by One Sigma Technologies and has previously faced investigation by the Enforcement Directorate (ED) for FDI and foreign exchange violations. The company reportedly received ₹913 crore under the guise of IT services, but ED found the actual business involved financial services, which require prior government approval-approval that was not obtained.

How BNPL Works

BNPL allows consumers to buy products instantly and pay later. At checkout, users can select the BNPL option and receive credit based on basic information or credit score checks. Payments can be made in installments or after a fixed period, often interest-free or with minimal fees. BNPL companies like Simpl earn merchant fees while providing flexible payment options to customers. However, defaults put the company at financial risk.

RBI's Clear Message

This case mirrors last year's action against card networks for operating third-party B2B payments without a license. The key issue in both cases is clearing and settlement without regulatory approval. RBI emphasizes that all digital payment systems, whether card-based or BNPL, must comply with its rules.

Company's Response

A Simpl executive stated that the company uses its own funds and no public money is involved. Losses in case of defaults are borne by the company, and they do not charge interest. Simpl earns merchant fees and late fees to avoid customers being trapped in interest cycles.