Last week I was at SVPNPA, my Alma Mater-the IPS training academy-to address the opening session of an in-service course on cybercrime, where I discussed the cybercrime ecosystem and the roles and responsibilities of police officers, with bright serving officers, we grappled with the threat landscape, the shifting trends, the actors, and their motives.

This article is a result of those deliberations.

The "perfect crime" was once a slow-burning affair-forged signatures, paper trails, a patient decay of evidence-but in the digital corridors of modern India, it has morphed into a high-velocity, industrial-scale operation. The traditional Lockheed Martin Cyber Kill Chain, that gold standard for breaching secure networks, feels like an artifact now-a relic when applied to the visceral reality of Indian financial fraud. Today, we see the "Indian financial kill chain," a hyperoptimized, mobile-native pipeline where the target is not some server's firewall, but the human psyche; the weapon is no complex zero-day exploit, but a simple, authorized, yet unintended transaction. It is a cognitive breach, a glitch in trust. As UPI payments become the lifeblood of the economy, a sophisticated shadow infrastructure has emerged to exploit it, moving from first contact to cross-border laundering in under an hour. This is no longer mere theft; it is a systemic extraction, a probabilistic nightmare where technology and desperation converge. The crime does not hide in the shadows but operates in plain sight, utilizing the very tools of progress to facilitate a seamless, digital disappearance of wealth into the abyss-fast, efficient, and utterly clinical.

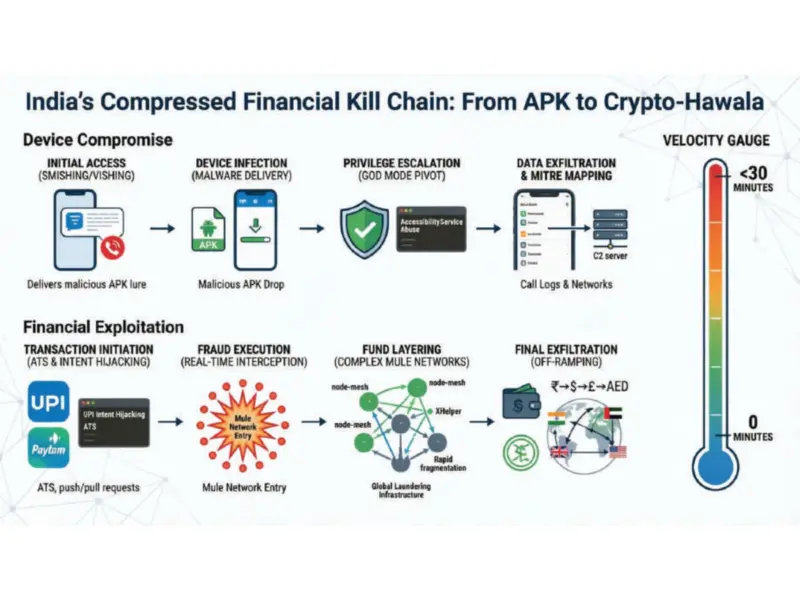

The architecture here is built on "Stage 0," a meticulous pre-exploitation that treats crime as a data-driven enterprise. Attackers no longer spray-and-pray; they construct risk-weighted victim graphs, harvesting leaked data from job portals, social media, and non-banking financial companies-this allows for a chilling precision in targeting salaried professionals or those seeking economic opportunity. While victims are profiled, the infrastructure is staged in parallel. Syndicates engage in bulk acquisition of "mule accounts"-bank accounts rented from the economically vulnerable-and register pseudo-merchants to generate legitimate-looking UPI handles. By the time the first message arrives, a directed acyclic graph of multi-hop routing is already primed to whisk away the proceeds.

Entry into this chain is rarely technical; it is a "cognitive compromise." The most pervasive innovation is "Digital Arrest" pretexting-advanced social engineering that weaponizes the weight of state authority. Scammers impersonate officials from the CBI or Narcotics Bureau, isolating victims through prolonged video calls and coercing them to "verify" funds by transferring them to designated accounts. In other scenarios, the hook is a technical payload via Smishing-SMS messages disguised as urgent tax refunds or KYC updates. These lead to malicious Android APKs, often through WebAPKs that bypass security warnings-tools from a modular "Digital Lutera" toolkit designed to subvert device trust entirely.

The technical core rests on the abuse of Android's Accessibility Services. Once a victim grants this permission-perhaps under the guise of a "security update"-the malware gains "God Mode." It can read screens, log keystrokes, and intercept SMS-based OTPs, granting the attacker physical-level control over the device. This allows for an Automated Transfer System (ATS), where malware initiates and approves UPI transactions in the background without user awareness. Such evolution renders "SIM-binding"-the idea that a bank account is tethered to a physical SIM-functionally obsolete, as the malware manipulates the operating system to report fabricated telephony states.

Once funds are extracted, the chain shifts into a "layering and churning" phase of breathtaking velocity. Stolen money is never stationary; it moves through a dense web of mule accounts, fragmented into sums under Rs 50,000 to evade algorithmic detection. This process is managed by illegal payment gateways-shadow platforms like PoccoPay or PeacePay-providing "Money Laundering-as-a-Service" to transnational syndicates. These gateways act as fraud transaction routers, optimizing throughput and minimizing alerts by distributing exposure across thousands of accounts. The efficiency is industrial: a platform like XHelper was found managing over 40,000 mule accounts, processing millions of dollars in mere days.

Finality arrives through "value conversion," turning electronic rupees into unlinked, consumable assets. While gold purchases and ATM cash-outs remain common, the dominant exit strategy has shifted toward cryptocurrency. Layered funds are converted into stablecoins like USDT via P2P exchanges operating with weak oversight. This digital value is then moved to offshore hubs in lax jurisdictions-Cambodia or Dubai-where it integrates into the international financial system. Often, this path converges with traditional "Hawala" networks, creating a hybrid system where crypto handles cross-border settlement while local ledgers are reconciled through encrypted messaging apps.

The resilience of this system is perhaps its most troubling feature, a hydra-headed persistence that defies traditional containment. It is a polycentric, low-cost ecosystem where the "mule," though ostensibly the weakest link, is also the most renewable resource-a human commodity in a digital market. Economic desperation provides a constant, flowing supply of individuals willing to rent their identities for small commissions; thus, even if law enforcement freezes thousands of accounts, the infrastructure regenerates almost instantly-germinating anew from the soil of poverty. Furthermore, because transactions are "authorized"-using the victim's own credentials and device-the legal recovery becomes a labyrinth of frustration, as post-facto repudiation is rendered exceptionally difficult. To the syndicates, funds frozen by authorities are not losses but mere operational costs-a predictable tax on a high-volume business model, an inevitable friction in a machine designed for absolute extraction.

Disrupting this modular pipeline requires us to move beyond the sterile limits of traditional endpoint security toward "behavioral analytics" and a state of real-time coordination-a shift from watching the door to understanding the dance. There are emerging hooks for intervention-the National Cyber Crime Reporting Portal (I4C) and proposed "kill switches" for banking apps-designed to allow instant freezes when fraud is suspected, cutting the circuit before the money vanishes. Tools like MuleHunter.AI now identify anomalous subgraphs in transaction patterns; they spot the exact moment a thousand unrelated users begin funneling money into one small, dense cluster of accounts-a digital fingerprint of theft. However, we are fighting against the clock. With more than half of all scams completing their entire cycle within twenty-four hours, the speed of response remains the critical bottleneck, a race where the adversary is always a heartbeat ahead.

The Indian financial kill chain is no longer just a series of isolated thefts; it has evolved into a sophisticated socio-technical system-a predatory architecture that weaponizes the very convenience of India's digital infrastructure against its own citizens, exploiting the trust embedded in the UPI ecosystem. We are witnessing a collision of code and psychology, where efficiency becomes the enemy. The challenge for the next decade will be to build a "defensive kill chain" as adaptive, fluid, and high-velocity as the threat it seeks to neutralize-a mirror image of the attack itself. This requires a coordinated effort spanning mobile OS hardening, telecom security, and aggressive enforcement against the laundering networks and illicit data brokers that fuel this shadow economy. Until the velocity of intervention matches the velocity of theft, the digital frontier remains a landscape of probabilistic risk, where the fastest hand wins-and the rest simply vanish into the void.

- Brijesh Singh is a senior IPS officer and an author (@ brijeshbsingh on X). His latest book on ancient India, "The Cloud Chariot" (Penguin) is out on stands. Views are personal.