The Reserve Bank of India and the Union government have both reduced India's growth projection for 2026-27 to 6.6% - which is still higher than the 6.2% annual growth rate achieved over the last 10 years.

The challenge before India is not merely to grow, but to do so more inclusively, and to grow faster and long enough to escape the middle-income trap.

Therefore, achieving the vision of Viksit Bharat (Developed India) requires sustaining GDP growth above 8% annually over the next two decades at least - a feat accomplished only by China so far. Such growth cannot be driven by 43% of the workforce still dependent on agriculture, and low-scale (micro and small) informal sector enterprises that still account for 90% of the Indian workforce.

India’s quest for Viksit Bharat 2047 is unfolding against the backdrop of a rapidly deteriorating global order and worsening climate change-related disruptions to growth, especially heatwaves and uncertain monsoons. Also, trade disruptions, geopolitically-driven economic sanctions and energy price volatility threaten to dampen India's export growth, constrain employment generation and intensify inflationary pressures.

In the face of such shocks, it will be difficult to create 12-13 million (1.2-1.3 crore) new non-farm jobs that India needs every year while sustaining 8% annual economic growth. These shocks weaken labour demand, raise the cost of living and suppress household consumption.

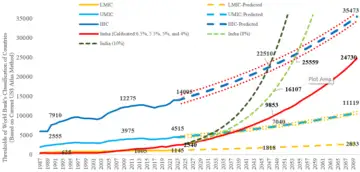

In an estimate in our recent book India Out of Work: Rethinking the Growth Story, and in figures that we updated recently, we caution that even sustained 8% GDP growth may be insufficient to secure high-income country or HIC status for India. This is because the global income threshold itself rises over time. The World Bank’s HIC threshold is not a fixed benchmark but a moving target, revised annually to reflect global inflation, exchange-rate movements and rising world incomes (see figure below).

Thresholds of World Bank's classification of countries and projections for India (per capita Gross National Income, current US $)

The indigo solid line in the figure above displays the threshold of HIC, which was at per capita Gross National Income (GNI) of $8,000 (based on World bank's Atlas method) during 1990. This moved up to about $12,200 during 2010, and further to $14,000 during 2025.

The indigo dashed line is our projection of the threshold of HIC in 2047 - at $22,500 - a big target indeed. By 2070, this threshold would be around $35,500.

Similarly, as the light blue solid and dashed lines in the figure above show, the threshold of Upper-Middle-Income-Country (UMIC) is projected to move up from $4,500 to about $7,040 during 2025 to 2047. It will move further up to $11,119 by 2070.

Hence, India remains vulnerable to the middle-income trap due to incomplete structural transformation, persistent dependence on low-productivity employment, rising informalisation and the unpaid family labour (UFL) phenomena, weak female participation in non-farm employment and poor human capital. Hence, growth alone will not deliver Viksit Bharat.

India needs 10% per annum non-stop growth of per capita GNI for the next 21 years to become a HIC by 2047 - the deep blue dashed line on the graph. However, if India could achieve and sustain 8% per annum growth of GNI per capita for the next 21 years, it would still become an UMIC by 2047. The per capita GNI would then be $16,107 (light green dashed line).

An uninterrupted 8% per annum growth would help India to cross the HIC threshold by 2055.

But the realistic assessment of facts suggest that India had never ever achieved above 6.5% growth rate of GNI per capita for the last two decades. Hence, an optimistic calibration-based projection of GNI per capita is presented by the solid red line in our figure. The projection is of about 6.5% GNI per capita growth for the next 10 years, followed by 5.5% for another decade, 5% for the third decade and 4% thereafter until 2070.

This indicates that India could move up the income ladder - again from being a lower-middle to upper-middle-income country by 2040, but it would remain in the middle-income trap until 2070, with a per capita GNI of $24,730.

Hence, India must generate large-scale quality employment outside agriculture, accelerate manufacturing and modern services, enhance women’s economic participation and strengthen education, skills and health systems. Without such transformative changes, India risks exhausting its demographic dividend before fully realising its developmental potential.

Furthermore, India cannot invest its way to prosperity when consumers lack purchasing power, nor when savings and investment rates continue to drift downward. The gross capital formation rate, which ranged between 32 and 38% of GDP over 2004-14, fell and remained range-bound between 26 and 32% over 2015 to 2025. Meanwhile, the gross savings rate also fell, from 37% to 30% of GDP during the same period.

Given the sustained current account deficit, reflected in India's gap between savings and investment, India will also need capital from abroad.

Formidable impediments

The most formidable impediments to India’s aspirations lie not in external geopolitical shocks but within the structural weaknesses of its labour market. For instance, female workforce participation remains among the world's lowest in the world. Our estimates also suggest that, all else being unchanged, an increase in the workforce participation rate of women by 10 per centage points could boost GDP growth by a statistically significant one percentage point. This could follow primarily because it will boost aggregate domestic demand, but also as it could potentially extend India's demographic dividend (presently ends 2040).

On the other hand, the rising unemployment among educated young reflects a widening disconnect between educational attainment and labour market opportunities. Even more concerning is the expansion of the NEET population - young people who are neither in education, employment, nor training. This represents a substantial loss of productive potential in a country expecting the benefits of a demographic dividend.

Every year, about 12 million (1.2 crore) young people remain disconnected from education and employment reducing future productivity and weakening long-term growth prospects.

Human capital formation remains another major weakness. While educational enrolment has expanded significantly, access to quality education remains deeply unequal across regions, income groups, caste categories and gender. The divide is even sharper in emerging areas such as science, technology, engineering, mathematics (STEM), artificial intelligence and advanced digital skills. Students from socially and economically disadvantaged communities often remain excluded from them.

Structural weaknesses within the production system further constrain India’s developmental trajectory. Informality dominates employment, leaving millions of workers trapped in low-productivity jobs with limited social protection. Simultaneously, India suffers from a persistent “missing middle” in enterprises. Millions of micro-enterprises coexist with a relatively small number of large corporations, while the growth of medium-sized firms remains constrained. This weakens innovation, productivity growth and the creation of quality jobs on the scale required.

The services sector, which has long been India’s growth engine, is no longer immune to disruption. Artificial intelligence is increasingly capable of performing many routine cognitive tasks that traditionally generated employment in IT, BPOs, finance, education and administrative services. As automation expands, future employment growth will increasingly depend on higher-order skills, creativity, innovation and continuous learning.

The assumption that the services sector alone can absorb even the best educated in India’s expanding workforce is becoming untenable; even IIT-ians face difficulties.

Without an industrial policy supplemented by an employment policy, the constrained aggregate demand will prevent private investment from reviving - a fact that policymakers have not been willing to recognise. Exhortations by various central ministers to corporates to increase private investment have not done the trick.

Meanwhile, to employ the young (6-7 million) who enter the labour force or are unemployed - all increasingly better educated, though they need better skills - India needs a manufacturing strategy that first focuses on labour-intensive goods for both the domestic and the export market. Surplus labour in agriculture needs millions of more jobs in construction, whether for infrastructure in cluster-based towns or urban low-cost housing or commercial space.

But the goods export potential cannot be realised merely by signing new Free Trade Agreements (FTA) - though they might help in the future - but by using the emerging five industrial corridors to plug into global value chains. If FTAs cannot help in this goal, their potential will remain unrealised.

Finally, the uncertain international security environment implies that India's development imperative now requires rapidly improving energy security - through nuclear capacity, faster solar/wind capacity development with storage and rapid growth in biomass-based distributed generation.

Therefore, the vision of Viksit Bharat ultimately depends on whether India can convert its demographic advantage into productive capabilities before the demographic window closes by 2040. The coming decade may prove decisive. In a world marked by geopolitical instability, technological disruption and slowing globalization, India’s journey towards becoming a developed nation is not merely a race for higher growth - it is a race against time itself.

Jajati Keshari Parida is Professor of Economics, University of Hyderabad, and Santosh Mehrotra is Visiting Professor, Higher School of Economics, Moscow.