India's informal sector accounts for roughly 45% of GDP (Gross Domestic Product), according to the Ministry of Statistics and Programme Implementation (MoSPI, 2025).

Low-income countries typically raise only 10 to14% of GDP in taxes, compared to 30 to 40% in high-income countries (Besley and Persson 2014). However, the consequences for India go beyond lost tax revenue: policy choices can sustain a dual economy in which small, unproductive firms exist alongside a distinct formal sector (La Porta and Shleifer 2014). Preferential treatment for small firms can reduce firms' incentives to invest in growing and in improving their productivity (Bento and Restuccia 2017). Prior to the GST (Goods and Services Tax) in India, firms below the excise threshold (Rs. 1.5 crore turnover) were exempt from tax, while state-level thresholds allowed smaller firms to operate outside the tax net.

Value-added tax (VAT) has an elegant property that speaks directly to this problem. The buyer wants a tax credit. To get it, they needs an invoice from a registered supplier. The supplier, in turn, wants credits from their own suppliers. Each firm in the chain has a private incentive to demand documentation from the firm behind it. The tax structure ensures that the tax enforces itself. The Kelkar Task Force Committee (2004) made this the central argument when it first proposed a comprehensive GST for India. de Paula and Scheinkman (2010) conceptualised this idea with a model of "formalisation cascades". Pomeranz (2015) provided experimental evidence from Chile that the credit mechanism deters evasion. But how does formalisation actually propagate through supply chains in emerging economies? In new research (Patnaik 2026), I bring the first empirical evidence on how formalisation cascades start with large firms and propagate upstream, following India's GST reform of 2017.

The pre-GST system and GST's self-enforcing design

Prior to July 2017, India's indirect tax system consisted of multiple overlapping layers: central excise duties on manufacturing, state-level VAT on within-state sales, and the Central Sales Tax (CST) on interstate transactions. CST was non-creditable: VAT credits were blocked across state lines. Thus, when a manufacturer purchased inputs from another state, CST of 2-4% was levied without credit, and excise duty was then levied on the full value including the embedded CST, and state VAT was levied on top of both. The cumulative effective rate could substantially exceed the sum of the statutory rates. In response, firms had restructured supply chains to minimise interstate transactions, established redundant facilities across states, and purchased from unregistered suppliers to avoid documented tax burdens.

GST replaced this fragmented system with a unified destination-based tax. Credits became available for all business inputs: goods or services, both within-state and interstate. The ability to claim input tax credit under GST is contingent on the supplier being registered and having reported the corresponding sale in their GST return, creating a direct linkage between buyer and seller (Gadenne, Nandi and Rathelot, forthcoming).

Firm-level evidence

Using CMIE (Centre for Monitoring Indian Economy) Prowess data on 12,024 firms over 2013-2022, I exploit heterogeneity in firms' pre-GST exposure to cascading taxes in a difference-in-differences framework. This involves comparing input tax credit and cost of materials among firms with different levels of exposure to cascading taxes, that would be differentially affected by the introduction of GST. The median firm paid indirect taxes equal to 8.2% of raw material expenditures, but there is high variation across firms: interquartile range is 0.9-16.9%. Firms with higher exposure had stronger incentives to shift to formal, registered suppliers under GST.

I find that firms with high pre-reform exposure to cascading taxes increased documented input purchases by 6% and reduced indirect tax payments by 8% following the GST reform. The effects are concentrated among private Indian firms in manufacturing, where informal procurement and multi-stage cascading were most prevalent. Government companies and foreign subsidiaries, already subject to heavy auditing, show no change.

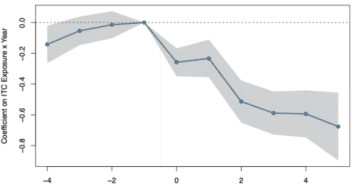

Figure 1 shows the 'event-study' estimates for indirect taxes: pre-reform coefficients are close to zero, and effects grow steadily over the five post-reform years. The effects roughly doubled between the first and fifth post-reform year. This is consistent with sequential propagation: firm A demands invoices from firm B, firm B then demands invoices from firm C, and so on upstream. The growing trajectory rules out one-time accounting reclassifications and provides the first empirical evidence of VAT-driven formalisation cascades at national scale.

Figure 1. Effect of input tax credit exposure on indirect taxes

Years Relative to GST (2017). Source: Patnaik (2026). Notes: (i) Figure plots coefficients from event-study regressions on interactions between exposure and year indicators. (ii) All specifications include firm fixed effects and industry × year fixed effects. (iii) The reference period is k=−1, corresponding to the fiscal year April 2016-March 2017 (the last pre-GST year); k = 0 is April 2017-March 2018 (the first post-GST year). (iv) Shaded areas show 95% confidence intervals based on firm-clustered standard errors. A 95% confidence interval means that, if you were to repeat the experiment with new samples, 95% of the time the calculated confidence interval would contain the true effect.

Macroeconomic figures suggest that the cascade starts with large, formal firms, the firms in the Prowess sample that are already in the tax net and have the strongest incentive to claim input credits. The share of national GST collections from India's largest firms (in the Prowess sample) fell from 46% to 30% - implying that collections from smaller, previously less formal enterprises grew faster. This is consistent with the hypothesis that these large firms demand invoices from their suppliers, and those suppliers face pressure to register under GST. Once registered, those suppliers in turn demand documentation from their own upstream providers. The formalisation thus propagates from the largest firms in the formal sector outward into the informal economy, with each layer of the supply chain pulling the next into the tax net. The initial effect is comparable in magnitude to what Pomeranz (2015) found from randomised audit threats in Chile, except the GST mechanism for India keeps growing as formalisation propagates upstream and exceeds the average estimates of Pomeranz (2015), making a case for self-enforcing mechanisms over audit and monitoring measures.

The spread of effective tax rates (the ratio of indirect taxes paid to raw material expenditures) across firms fell by 72%, meaning GST made the tax burden far more even across firms. Uneven tax burdens distort input prices and cause resources to be allocated inefficiently across firms - the kind of misallocation Hsieh and Klenow (2009) documented for India and China. This narrowing of tax rate differences meant that firms could make input choices based on productivity rather than on which supplier happened to generate a lower tax burden. My estimates are likely a conservative lower bound on GST's true impact, since the sample I use only covers firms that were already formal, so gains from firms that entered the formal economy after GST are not captured. Given how many firms moved out of the informal sector, the spread of effective taxes probably shrank even more.

Megha Patnaik is an Assistant Professor in the Department of Economics & Finance at LUISS Guido Carli University and a Research Affiliate at the Centre for Economic Policy Research and CESifo Institute.

This article originally appeared on Ideas for India and has been republished with permission.