Roughly 80% of everything traded on earth travels by sea. The phone in your hand, the grain in your bread, the fuel in your car-it's all moving across the oceans right now.

What almost nobody thinks about is just how little room all of this has to move. The past 18 months have been an unusually sharp reminder of this. One passage has been effectively restricted. Another is now under threat. A third quietly ran into a drought it had no defence against. The system is visibly under strain.

On June 1, Brent crude jumped more than 4% to around $95 a barrel after Tehran said it would fully block the Strait of Hormuz as well as the Bab-el-Mandeb Strait, off the coast of Yemen. No ship was sunk and no cargo was seized; a few words were enough to move the price the world pays for energy.

Here is what each passage carries, where the vulnerability lies.

The critical trade "chokepoints"

| Chokepoint | What flows through | Impace / Scale | Core vulnerability |

|---|---|---|---|

| Strait of Hormuz | Crude oil, LNG | ~20-21 mb/d oil; ~20% of world oil use; ~20% of LNG | Military conflict; few alternatives |

| Strait of Malacca | Oil, LNG, manufactured goods | ~23.2 mb/d oil (~29% of seaborne oil) | Congestion, piracy, China-US friction |

| Suez Canal | Containers, energy, finished goods | ~12-15% of global trade; ~30% of containers | Red Sea conflict; accidental blockage |

| Bab-el-Mandeb | Gateway feeding the Suez | Oil fell from ~9.3 → ~4 mb/d since 2023 | Attacks on shipping; Yemen conflict |

| Taiwan Strait | Semiconductors, electronics | >20% of seaborne trade; ~half the container fleet (2022) | Geopolitical confrontation |

| Panama Canal | US grain, LNG, chemicals | ~5% of global maritime trade; ~40% of US containers | Drought / low water levels |

| Turkish Straits | Grain, fertiliser, Russian oil | Key Black Sea artery | Regional war; transit rules |

Sources: U.S. Energy Information Administration, World Oil Transit Chokepoints (March 2026); International Energy Agency; UN Trade and Development (UNCTAD), Review of Maritime Transport 2024; IMF PortWatch; Center for Strategic and International Studies (CSIS); Panama Canal Authority.

The energy gates

Strait of Hormuz

If there is a king of chokepoints, this is it, and it needs no introduction. The narrow channel between Iran and Oman carries ~20-21 million barrels of oil a day. The uncomfortable truth is that there is no real Plan B: bypass pipelines in Saudi Arabia and the UAE could reroute only a fraction if the Strait is shut.

Strait of Malacca

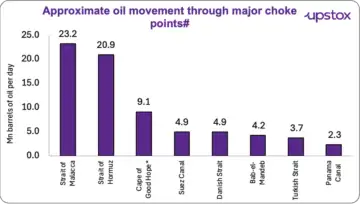

Less famous than Hormuz, but by oil volume even busier. The slim corridor between Indonesia, Malaysia and Singapore is the shortest route between Middle Eastern energy and the factories of East Asia. It handles ~23.2 million barrels a day - equivalent to about 29% of all seaborne oil flows. China alone accounted for 48% of the crude passing through.

Strategists call China's reliance here the "Malacca dilemma". One congested, piracy-prone strait stands between the world's second-largest economy and its energy supply. Rerouting around Indonesia is possible, but it adds days and billions of dollars.

How much oil moves through each chokepoint

Source: US Energy Information, World Transit Chokepoints; *Cape of Good Hope is not a checkpoint but the main detour route around Africa; # Basis latest avialble data

The trade gates

Suez Canal

Egypt's man-made shortcut between the Mediterranean and the Red Sea is the spine of the Asia-Europe supply chain. It handled roughly 12% to 15% of global trade. Anyone who remembers the Ever Given - the giant container ship that wedged itself across the canal for six days in 2021 - knows how a single stuck vessel can jam global commerce.

Bab-el-Mandeb Strait

This is the gate now in the headlines. It matters because of geography: ships cannot reach the Suez Canal from the Indian Ocean without first threading the Bab-el-Mandeb, the roughly 20-mile-wide channel between Yemen and the Horn of Africa. Block it, and the Suez becomes a road to nowhere.

The diversions have already happened once. As attacks on Red Sea shipping mounted from late 2023, oil moving through the strait collapsed - from about 9.3 million barrels a day in 2023 to roughly 4 million by 2025 - as tankers chose the long way round Africa instead.

Panama Canal

The odd one out. The waterway linking the Atlantic and Pacific handles around 5% of global maritime trade. The US is by far its largest user, with roughly 40% of all US container traffic and about $270 billion in cargo passing through each year. Its biggest enemy is not a navy but the weather: the locks run on freshwater from a single lake, and a historic drought cut transits by about 29% in the 2024 fiscal year. It is the rare chokepoint where the risk is slow, visible and seasonal rather than sudden.

The flashpoint gates

Taiwan Strait

Quietly, one of the most important stretches of water on Earth. More than 20% of the world's maritime trade passes through it - energy, electronics and minerals - crossed these waters.

A significant share of global container traffic passes through the strait. It is also the artery for the advanced semiconductors that the entire technology industry depends on. Any serious confrontation here would not merely lift freight rates - it would reach the chips inside almost everything electronic.

Turkish Straits (Bosphorus and Dardanelles)

This is the Black Sea's only door to the Mediterranean, and therefore the route for a large share of the world's wheat, fertiliser and Russian oil. Because so much grain flows through here, disruption tends to surface not at the petrol pump but at the dinner table - a food-security story before it is an energy one.

But why are workarounds so limited?

If a short cut on your way to work is shut, there is always another route you can take. The only result is - it would take longer and cost more. It's the same with these points. There have always been workarounds, alternate routes that can be taken, in case a chokepoint is under risk.

But as you would guess, it increases the time and cost. Take the Suez Canal for example, if shut, ships can always go around the Cape of Good Hope, but that would add anywhere between 10-15 more days on Asian-European routes.

The traffic does not stop; it bends. Longer voyages tie up ships for longer, which shrinks the effective fleet and pushes up freight rates and fuel bills.

How should investors read this

| If this breaks | What to look out for |

|---|---|

| Hormuz | Oil prices, INR, inflation |

| Suez | Freight rates, delivery delays |

| Panama | US logistics, agri exports |

One simple model helps tie it together: think in chains, not points. Hormuz leads to oil, which leads to inflation, which leads to central banks. Bab-el-Mandeb leads to the Suez, which leads to Europe's supply chains. Panama leads to US logistics, which leads to retail shelves. The water is narrow; the consequences are anything but.

Disclaimer: Views and opinions expressed in the article are the author's own and do not reflect those of Upstox. Stocks and securities mentioned are illustrative and not recommendations. Please consult a registered financial advisor before making any investment decision.